5 Ways Credit Unions are Different than Banks

As people increasingly appreciate local, cooperatively owned businesses, more Iowans are shopping for alternatives to big banks. As financial cooperatives, credit unions have become an increasingly popular choice due to their lower (or no) fees, better interest rates and personable customer service.

Although both entities offer similar financial services, they operate much differently. Here are a few key differences between credit unions and banks.

1. Credit unions are not-for-profit, financial cooperatives.

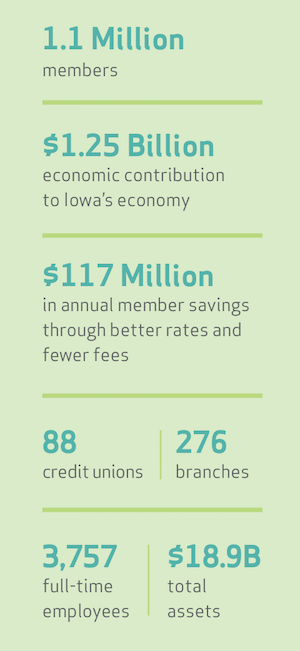

Banks are for-profit financial institutions. Profits go to select shareholders. Credit unions are democratically controlled, not-for-profit financial cooperatives, owned equally by all members they serve. 1.1 million Iowans are credit union members. Each member has one ownership share and gets one vote in electing the board of directors.

They reinvest their earnings to provide all members with the most affordable financial services in the form of lower fees, higher interest rates on savings and lower rates on loans. The Iowa Credit Union League estimates the state’s credit union members save $117 million annually compared to what they would have paid for similar services at a bank.

Here’s how to find a credit union near you.

2. Credit unions help people when banks won’t.

Credit unions help Iowans and small business owners that often aren’t served by banks. Because credit unions’ goal is not to create profits for shareholders, but rather to help members improve their financial lives, they evaluate loan applications on a case-by-case basis and are willing to take more chances in support of people needing help.

Iowa

3. Credit unions promote healthy competition.

Banks complain about competition, but credit unions serve as a check and balance in the marketplace. In that sense, all Iowans benefit from credit unions. Although credit union membership is growing, they remain a relatively small piece of the financial puzzle. Consider this:

- Wells Fargo alone is bigger than all 5,500 U.S. credit unions combined.

- In Iowa, banks control 85.2% of deposits and 95.7% of business loans.

- Iowa banks made $937 million in profits last year.

Healthy competition is good for consumers.

4. Credit unions pay taxes, too.

Iowa credit unions pay millions in taxes each year. They pay payroll tax, property tax, sales tax and a state “moneys and credits” tax on their legal reserves (which banks do not pay).

Despite their for-profit status, banks have found ways to substantially mitigate their tax liability. In Iowa alone, banks avoided more than 72% of state franchise tax liability in 2017 by taking advantage of tax credits. 183 Iowa banks have formed Sub-Chapter S corporations, which don’t pay corporate income tax. By organizing as Sub-Chapter S corporations, those banks avoided paying $65.1 million in federal corporate income tax.

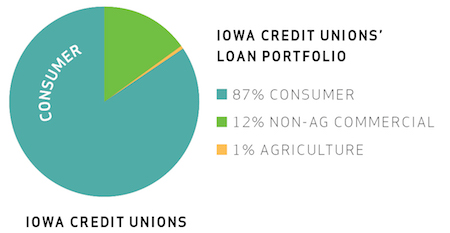

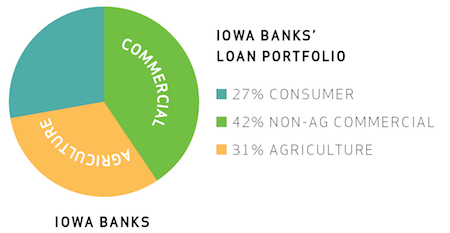

5. Credit unions are focused on consumers.

In Iowa, 87 percent of the credit union loan portfolio is comprised of consumer loans. In contrast, just 27 percent of Iowa bank loans are consumer loans.

Although credit unions and banks are different, banks are lobbying to increase taxes on credit unions so they are taxed the same as banks. If that tax increase were to happen, Iowans would see higher fees and less competitive rates on loans and other services.

Although credit unions and banks are different, banks are lobbying to increase taxes on credit unions so they are taxed the same as banks. If that tax increase were to happen, Iowans would see higher fees and less competitive rates on loans and other services.

To learn more about Iowa credit unions, and to stay informed on the legislative issues that affect your community credit unions, visit the Iowa Credit Union League (ICUL) at iowacreditunions.com.